What the Record Shows: Phil Scott

Nine years in office. Nineteen questions. The public record

Vermont Investigative transmitted a written questionnaire to Governor Phil Scott’s press office on May 16, 2026 — fourteen master questions asked of all nine statewide candidates, plus five candidate-specific addendum questions drawn from his record, stated positions, and public statements. The response deadline was May 30, 2026. Initial transmission to press@governor.vermont.gov encountered server delivery failures; the questionnaire was retransmitted to press secretary Amanda Wheeler at amanda.wheeler@vermont.gov. Both transmissions are documented.

Governor Scott announced his candidacy for a sixth term on May 24, 2026 — eight days after the questionnaire was transmitted to his office. No written response was received by the May 30 deadline. No extension was requested. No response has been received as of publication.

In the absence of written responses, Vermont Investigative reviewed the public record of his nine-year administration: budget addresses, press releases, public statements, official rulemaking filings, financial disclosures, and fiscal analysis by the Vermont Joint Fiscal Office. What follows is what those documents show, organized by question. Where the public record speaks, it is cited. Where it does not, that absence is noted.

Who Is Paying Him

Vermont Investigative reviewed three primary documents filed by or on behalf of Phil Scott in 2026: his candidate financial disclosure form filed May 26, 2026 under 17 V.S.A. § 2414; his 2025 federal income tax return filed jointly with his spouse Diana McTeague Scott; and his campaign finance disclosure statement covering June 29, 2025 through March 12, 2026.

Phil Scott’s 2026 Financial Disclosure form, filed with the Vermont Secretary of State on May 26, 2026, lists a single employer: the State of Vermont. No think tank. No foundation. No consulting relationship. No organizational affiliation requiring disclosure.

His IRS Form 1040 for tax year 2025, filed jointly with his spouse Diana McTeague Scott, shows:

Filing status: Married filing jointly

W-2 wages: $233,279 (governor’s salary)

IRA distributions: $143,750

Capital gains: $92,904

Dividend income: $21,448

Adjusted gross income: $508,164

Occupation listed: GOVERNOR

His spouse, Diana McTeague Scott, is a registered nurse and holds an ownership interest in VIDA Wellness on Main Street in Barre, Vermont.

There is no institutional network behind Phil Scott’s income comparable to the one documented in the Janoo piece. His financial picture is a state salary, arm’s-length managed investments, and his spouse’s small business in Barre. That is what the documents show.

Vermont Investigative makes no editorial judgment about his income level or financial situation. These are documented facts from public records he filed himself.

Investments

Individual stock holdings over $25,000 managed by Granite Financial Group, Barre, Vermont — an independent firm affiliated with LPL Financial, San Diego.

Scott states he gave the firm sole discretion to invest for greatest return and does not direct specific purchases.

Disclosed holdings include: Apple, Amazon, Broadcom, Alphabet (Class A and C), Eli Lilly, Meta, NextEra Energy, NVIDIA, UnitedHealth Group, Visa, Walmart, Taiwan Semiconductor, Baker Hughes, Caterpillar, Rockwell, L3Harris, Analog Devices, AMD, ATI.

No investment funds, trusts, virtual currencies, state bonds, non-commercial loans, or company ownership with state business disclosed.

2026 campaign finance

Total contributions as of March 15, 2026 filing: $4,095. Total expenditures: $23,780. Campaign operating on $218,728 surplus carried from prior cycles.

Two contributions over $100 disclosed: Anheuser-Busch, St. Louis, MO ($2,000, December 30, 2025); Scott Giles, Shelburne, VT ($250, March 11, 2026).

Anheuser-Busch is the only corporate donor in the 2026 filing period. In 2022, Scott signed HB 730, reducing Vermont’s excise tax on spirits-based ready-to-drink cocktails from $7.68 per gallon to $1.10 per gallon. Anheuser-Busch acquired Cutwater Spirits, a spirits-based ready-to-drink brand, in 2019. Vermont Investigative documents the sequence. No inference is drawn beyond what the public record shows.

Photo: U.S. Air National Guard / Tech. Sgt. Sarah Mattison — Public domain

The Questionnaire Record

The following nineteen questions were transmitted to Governor Scott’s office on May 16, 2026, along with five candidate-specific addendum questions. No written response was received to any of them. Where the public record addresses a question, it is documented below. Where it does not, that absence is noted.

Q1. The Housing Demand Number

What the public record shows:

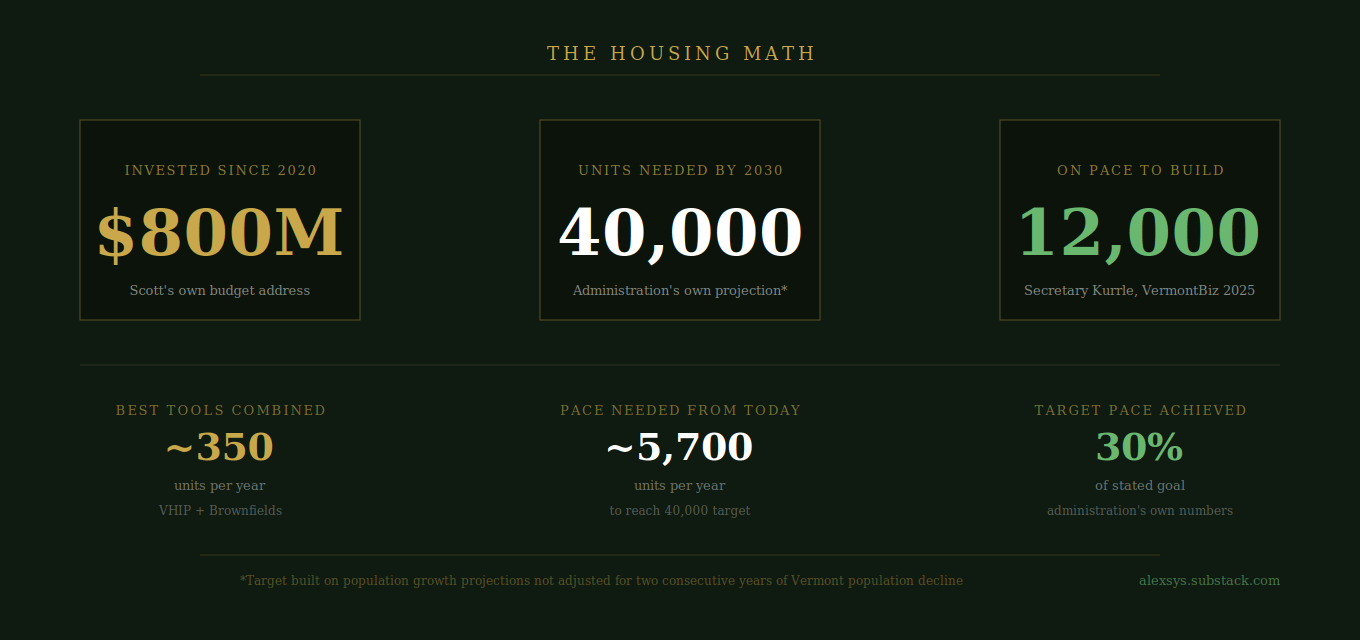

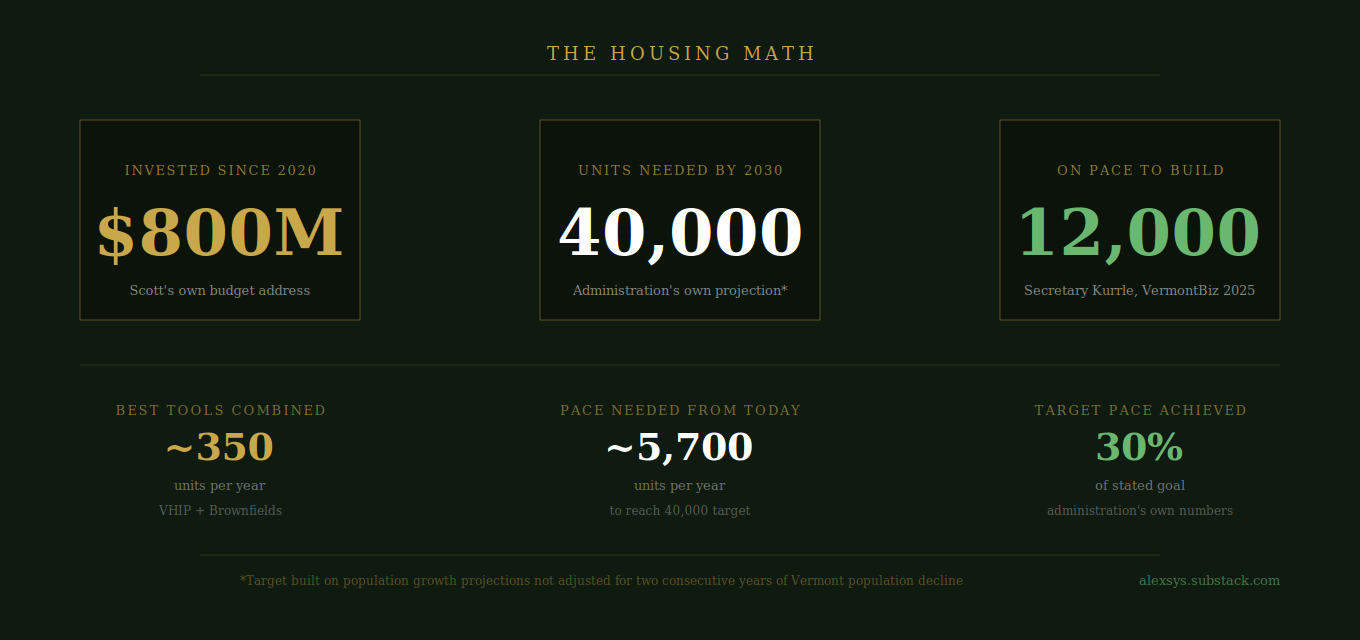

Scott’s January 20, 2026 budget address to the legislature: “investing nearly $800 million since 2020” in housing, with a remaining need of “about 30,000 homes over the next four years.”

Lindsay Kurrle, Secretary of Commerce and Community Development, in a September 2025 VermontBiz op-ed: “By 2030, the statewide demand for housing units will exceed 40,000. Right now, we’re on target to build just over 12,000.”

The administration’s own figures show Vermont on pace to produce approximately 30% of its stated target.

No public statement from Scott adjusting the demand projection to reflect two consecutive years of Vermont population decline or rising housing inventory.

What was asked: Whether the administration’s demand projection has been adjusted for population decline and rising inventory; whether the problem is primarily a supply shortage or a pricing mismatch in existing inventory. No written response was received.

Q2. Revenue Projections for Non-Primary Residence Taxation

What the public record shows:

Act 73, signed by Scott in June 2025, creates a new “nonhomestead residential” property tax classification targeting second homes, vacation properties, and short-term rentals, effective FY2029.

Department of Taxes reporting projects second home owners could face rates as high as $2.00 per $100 of property value, compared to $1.00–$1.30 for primary residences.

During the 2025 session, Scott opposed the standalone House version of the second home tax classification in H.454. The compromise Act 73 he signed included it as part of the broader education finance restructuring.

The Department of Taxes has acknowledged Vermont lacks the administrative infrastructure to implement the classification before FY2029.

No legal definition of “vacation home” or “second home” currently exists in Vermont tax code.

What was asked: The specific fiscal analysis — including assumed tax rate, taxable property value base, projected behavioral response, and implementation timeline — supporting the revenue projection for the new classification. No written response was received.

Q3. Education Fund Revenue Risk

What the public record shows:

Vermont’s Education Fund receives approximately 39% of its revenue from the nonhomestead property tax — $955.6 million of $2,432.6 million total Education Fund sources projected for FY2027, per the FY2027 Budget Summary, page 7, Education Fund Revenue by Component.

The nonhomestead residential classification created by Act 73 — signed by Scott — takes effect FY2029 and will apply substantially higher tax rates to second homes and vacation properties.

Vermont’s nonhomestead base includes not just second homes but commercial real estate, farms, and long-term rental properties — meaning behavioral response to the new classification has implications beyond the vacation home market.

No public record found of Scott addressing the Education Fund revenue risk specifically in the context of the new nonhomestead residential classification.

What was asked: What contingency mechanism Scott would pursue if increased tax rates reduce the number of non-primary-residence properties through sale, conversion, or market withdrawal, and what that does to Education Fund revenue. No written response was received.

Q4. Noncitizen Voting in School Budget Elections

What the public record shows:

Scott vetoed noncitizen voting charter amendments for Montpelier and Winooski in 2021, and for Burlington in 2023. His stated rationale from the Burlington veto message: “This highly variable town-by-town approach to municipal election policy creates separate and unequal classes of legal residents potentially eligible to vote on local voting issues. The fundamentals of voting should be universal and implemented statewide.”

The Legislature overrode all three vetoes.

On May 15, 2026 — the day before Vermont Investigative transmitted its questionnaire — the Vermont Supreme Court upheld Burlington’s charter amendment in a split decision. The majority held school budget votes are local matters not subject to the constitutional citizenship requirement. The dissenting judge argued school budget votes are statewide matters because they are funded through the statewide Education Fund supported by property taxes paid by all Vermont property owners — the same framing as the questionnaire.

As of publication, Scott has issued no public statement responding to the May 15, 2026 Vermont Supreme Court ruling.

News coverage of the ruling noted: if Scott’s district consolidation proposals under Act 73 produce the mandatory mergers he sought, Burlington and Winooski would cease to be standalone school districts, effectively making the noncitizen school budget voting question moot.

What was asked: Whether Scott supports expanding noncitizen voting in school budget elections to additional municipalities, and what legislative or constitutional remedy he would pursue. No written response was received.

Q5. Healthcare Funding Mechanism

What the public record shows:

Scott’s January 2026 budget address identifies healthcare as a defining crisis: Vermont has produced “some of the fewest choices and some of the highest costs in the nation” — the result, in his framing, of a failed single-payer pursuit and a regulatory framework that remains embedded in the system.

His proposed healthcare solution, as documented in his FY2027 budget address and budget summary, consists of: expanded insurance plan options for young people and working families; a reinsurance mechanism; and a federal Rural Health Transformation grant described as directing “nearly one billion dollars into rural health” over five years. No state funding mechanism is identified for any of these proposals beyond the federal grant.

The $1 billion rural health figure is federal money over five years — approximately $200 million per year in federal pass-through — not a Vermont state appropriation. Scott does not control this funding. It originates from a Biden-era federal initiative.

Scott’s own FY2027 budget address contains this statement about federal funding broadly: “even the traditional funding we’ve come to expect from Washington is uncertain.” His primary healthcare expansion mechanism depends entirely on the federal funding he describes as uncertain in the same document.

S.190, the reference-based pricing bill, passed the Vermont Legislature May 29, 2026 on a near party-line vote. The bill would give the Green Mountain Care Board authority to cap hospital prices for school employee plans and ACA marketplace plans. Scott’s administration signaled opposition before the vote. DFR Commissioner Kaj Samsom stated: “Nothing substantive is happening in this bill in terms of the cost to Vermonters in the aggregate, except for allowing the care board to concentrate those things in a way that we find objectionable.” As of June 8, 2026 — the last update date of the governor’s official 2026 legislative actions page — S.190 does not appear. No action has been taken. Vermont Investigative will update this section when action is confirmed.

No specific state funding mechanism, total annual cost, or independent fiscal analysis identified for any universal or expanded healthcare program in the public record.

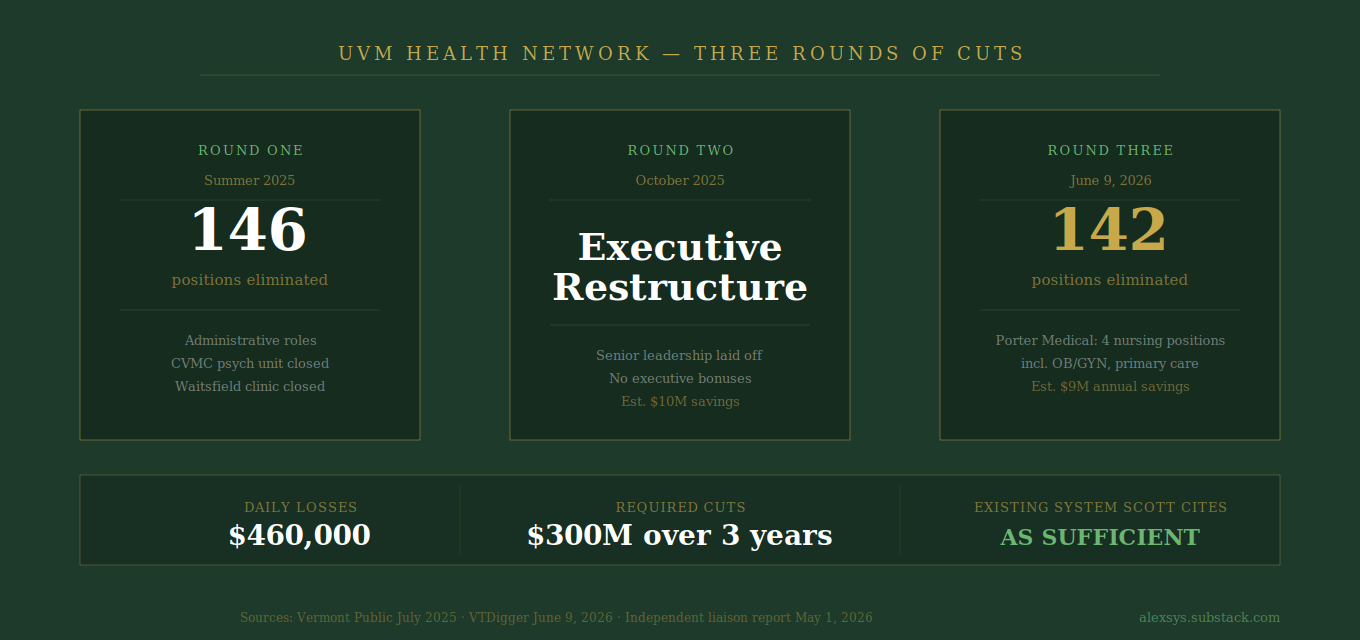

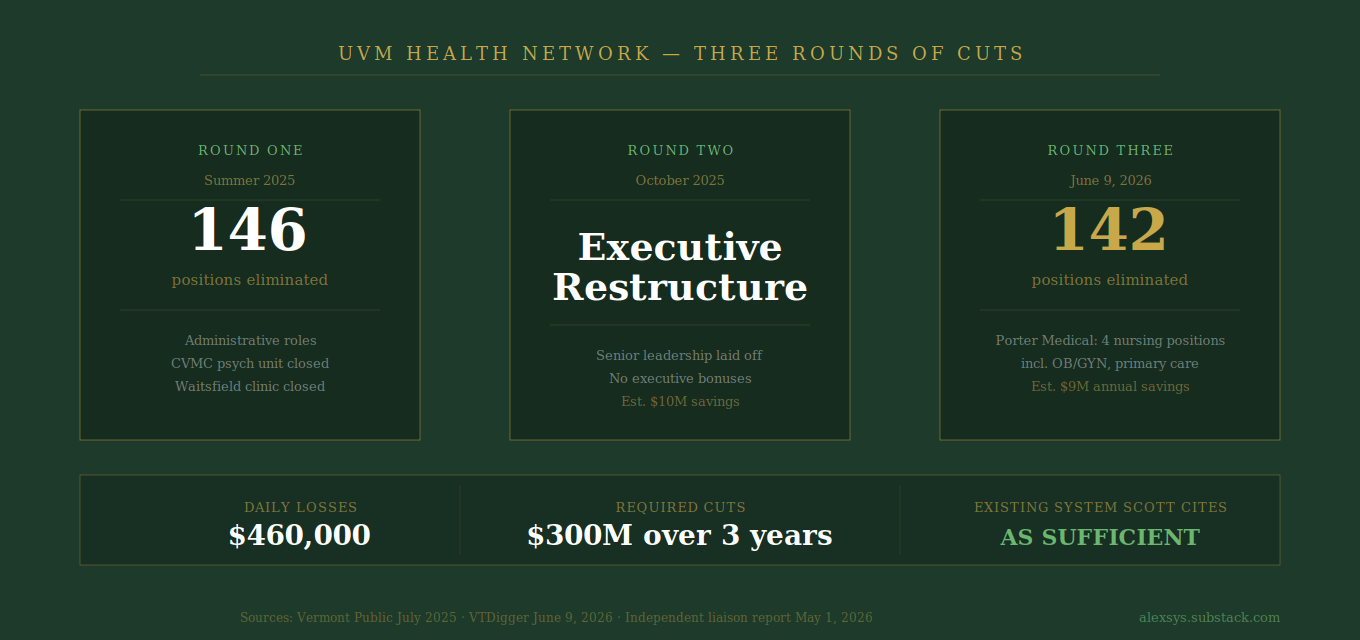

Vermont’s largest hospital system, UVM Health Network, has undergone three rounds of workforce reductions since summer 2025 under pressure from GMCB budget orders and declining revenue: 146 administrative positions in summer 2025; executive restructuring in October 2025; and 142 additional positions on June 9, 2026 — including four nursing positions at Porter Medical Center in Middlebury (three primary care, one OB/GYN). UVM Medical Center was losing $460,000 per day as of April 2026, per CEO Dr. Steve Leffler’s testimony to the legislature. An independent liaison report dated May 1, 2026 recommended the network cut $300 million over three years in preparation for reductions in Medicaid and commercial insurance revenue. Prior cuts have included closure of the inpatient psychiatric unit at Central Vermont Medical Center and primary care clinic closures in Waitsfield. Scott’s proposed Rural Health Transformation federal grant is directed at expanding rural healthcare access — while rural healthcare infrastructure is contracting under the existing regulatory system he cites as sufficient.

What was asked: Total annual cost of any universal or expanded healthcare program; specific funding mechanism; number of Vermont residents within the proposed funding threshold; projected annual revenue from that mechanism; and independent fiscal verification. No written response was received.

Q6. New Program Cost Totals

What the public record shows:

Scott’s FY2027 budget proposal totals $9.335 billion across all funds, approximately 3% more than the prior fiscal year. Baseline cost growth alone — inflation, pension obligations, and statutory commitments — totaled $139 million year over year before any new program spending, per the FY2027 Budget Summary.

Vermont Investigative reviewed the Governor’s FY2027 Budget Highlights on pages 8-9 of the Budget Summary against each stated initiative. What the document shows:

VHIP ($4 million base General Fund): Making permanent a program that already existed. Not a new initiative.

MHIR ($800,000 one-time): One-time money for an existing program.

Hotel/motel transition ($21.2 million one-time): A transition cost for winding down an existing program he is eliminating — not new spending.

Substance use shelters and case management ($10.2 million additional base): Redirecting existing hotel/motel money into a different delivery model.

Recovery employment program ($875,000 base): New, small.

Pre-trial supervision expansion ($200,000 base): Expanding an existing pilot statewide.

Community Accountability Court replication ($500,000 one-time): Replicating an existing Burlington pilot in additional counties.

CHIP: $0 in direct state appropriation. A TIF financing tool that leverages municipal and private investment. The $2 billion figure is projected leveraged investment over a decade, not a state expenditure.

Downtown and Village Tax Credits: Existing program. Scott proposes continuing support, not creating it.

Of the initiatives Scott identifies as new in his budget highlights, the only genuinely structural innovation is CHIP — and it carries no direct state cost. The remainder are existing programs made permanent, existing programs redirected, existing pilots replicated, or transition costs for programs being eliminated.

Scott’s budget address is explicit about the constraint: “Gone are the days of saying yes to every group asking for more funding” and “funding alone doesn’t fix broken systems.”

What was asked: Each new spending initiative, its annual cost, its funding source, and the total net new cost to Vermont taxpayers. No written response was received.

Q7. Cuts and Offsets

What the public record shows:

VTrans workforce reduction: The Agency of Transportation eliminated 31 positions in September 2025, then proposed an additional 20 positions in January 2026. Transportation Secretary Joe Flynn told lawmakers the combined reductions save approximately $7.5 million annually. The 20 January positions targeted maintenance districts across the state’s nine regions. Vermont Public reported this directly from Flynn’s legislative briefing, January 21, 2026.

Hotel/motel emergency shelter program: Scott’s FY2027 budget address explicitly calls for ending the hotel/motel voucher program — “the hotel/motel program has not worked. Even with the best intentions, it’s done more harm than good” — redirecting funding to emergency shelters with wraparound services. No specific annual savings figure stated in the budget address.

JTOC transfer elimination: Scott’s budget addresses in both FY2026 and FY2027 identify ending the Job Training Opportunity Center transfer — described in his FY2026 address as something “some of us have been trying to do for decades” — as a structural Transportation Fund repair. The $10 million reduction in the Purchase and Use tax transfer in FY2027 is a step in that direction. No single-year savings figure aggregated for both actions in primary documents reviewed.

FY2026 base spending reductions: At Scott’s insistence, the Legislature cut approximately $21 million in base spending from the FY2026 budget before he signed it in May 2025. VTDigger reported Democratic leadership trimmed recurring expenditures knowing they could not override a veto.

Education consolidation under Act 73: Scott’s stated position is that Act 73 district consolidation produces long-term structural savings — but no specific dollar figure for consolidation savings has been stated publicly in primary documents reviewed.

Transportation Fund structural deficit: Scott’s FY2027 budget address acknowledges a $33 million structural deficit in the Transportation Fund and directs AOT to manage through workforce and project reductions.

What was asked: The single largest spending reduction, program elimination, or structural reform his administration would pursue, the estimated savings, and the mechanism. No written response was received.

Q8. Act 59, 30x30, and Conservation Finance

What the public record shows:

Scott allowed Act 59 — Vermont’s 30x30/50x50 conservation legislation — to become law without his signature in June 2023. His public statement at the time did not endorse or oppose the bill’s conservation targets.

March 26, 2026: Scott’s official governor’s blog published a commentary by Sam Lincoln, former Deputy Commissioner of the Vermont Department of Forests, Parks and Recreation under Scott. The piece argues Vermont’s land use regulatory process has “disregarded or actively worked against” rural Vermonters, that “paid advocates have had a disproportionate voice in shaping outcomes,” and states: “If legislation affects landowners, they belong at the center of the process — not relegated to public comment sessions after the big picture policy decisions have been made.” And directly: “No more decisions about rural Vermont without rural Vermonters at the table.” Scott chose to publish this commentary on his official platform. It represents the administration’s framing of the working lands versus conservation regulatory tension.

May 12, 2026: Scott publicly supported H.70, a bill that would have counted land enrolled in Vermont’s Current Use program — the state’s working lands tax incentive for farms and forests — toward Act 59’s 30x30/50x50 conservation goals. The House voted against bringing the bill to the floor. Scott posted on Facebook: “If they had been successful, I believe H.70 would clarify the important role farmers, foresters and rural landowners play as stewards of Vermont’s land.” H.70 represents a direct documented position on how Act 59 conservation goals should be measured — specifically that working farms and forests should qualify alongside land held under conservation easements or formal protection.

No public statement found on the use of carbon markets or biodiversity offset markets to fund Act 59 goals specifically. However, Scott’s climate omnibus bill H.289, introduced February 2025, proposes switching Vermont’s emissions accounting from a gross to a net system — which would allow Vermont’s forests and working lands to count as carbon offsets against the state’s emissions obligations. Net accounting is the foundational methodology underlying carbon credit valuation. Scott has not addressed whether that accounting framework would extend to tradeable carbon credits or Act 59 conservation finance mechanisms.

No public statement found on restrictions for foreign institutional investment in Vermont land or conservation easements.

What was asked: Whether he supports carbon or biodiversity offset markets for Act 59 funding; which entities would be eligible to purchase or hold credits; what restrictions would apply to foreign institutional investment; and how his administration would ensure conservation finance targets do not lock rural Vermont land out of agricultural or working forest use. No written response was received.

Q9. Natural Capital Valuation and the Monetization of Vermont Land

What the public record shows:

No public statement found of Scott using the terms “natural capital,” “biodiversity credits,” “ecosystem services markets,” or addressing the monetization of Vermont land as a tradeable asset class. That vocabulary does not appear in his public record.

His official governor’s blog published a March 26, 2026 commentary by Sam Lincoln, former Deputy Commissioner of Forests, Parks and Recreation under Scott, addressing the underlying structural concern in different terms: “paid advocates have had a disproportionate voice in shaping outcomes” and “if legislation affects landowners, they belong at the center of the process — not relegated to public comment sessions after the big picture policy decisions have been made.” Scott chose to publish this on his official platform. It addresses who controls and who benefits from Vermont conservation policy — but does not address conservation finance instruments or the monetization of land as a financial asset.

Scott’s climate omnibus bill H.289, introduced February 2025, proposes switching Vermont’s emissions accounting from a gross to a net system — which would allow Vermont’s forests and working lands to count as carbon offsets against the state’s emissions obligations. Net accounting is the foundational methodology underlying natural capital valuation: it assigns a quantified value to a forest’s carbon sequestration capacity. That is natural capital accounting in its most basic documented form. Scott has not addressed whether that framework would extend to tradeable credits, who would hold or benefit from those credits, or what protections would apply to Vermont landowners.

His support for H.70 — which would have counted Current Use working lands toward Act 59’s conservation targets — reflects a position that the benefit of Vermont’s conservation system should accrue to working landowners rather than exclusively to conservation organizations. It does not address financial instruments or foreign capital.

No public record found of Scott addressing what protections would prevent conservation finance from accelerating transfer of land stewardship from Vermont families to institutional investors or foreign capital.

What was asked: Whether he supports applying natural capital valuation frameworks to Vermont land, who benefits when a Vermont wetland or forest becomes a tradeable credit, and what protections his administration would establish to prevent conservation finance from accelerating transfer of land stewardship from Vermont families to institutional investors or foreign capital. No written response was received.

Q10. Land Ownership, Absentee Control, and Easement Transparency

What the public record shows:

Scott’s public record on land ownership focuses consistently on protecting Vermont landowners from regulatory overreach — his vetoes of Act 181 and noncitizen voting charter amendments, his working lands commentary, and his H.70 support all frame the concern as state and conservation organization authority overriding landowner rights.

That framing addresses one direction of the land control question — state regulatory power over private owners — but does not address the other direction: whether conservation easements held by out-of-state nonprofits, national land trusts, or entities with foreign capital interests represent a form of absentee control over Vermont land use that warrants similar scrutiny.

No public record found of Scott addressing conservation easement holder transparency, disclosure of easement funder sources, or whether Vermonters have a right to know when international capital has a financial interest in Vermont land through easement structures.

The H.70 bill Scott supported would have counted Current Use working lands toward Act 59 targets — but did not address easement holder disclosure or foreign capital interests in conservation structures.

What was asked: Whether his definition of problematic land control extends to conservation easements held by out-of-state nonprofits or national land trusts; whether he supports public disclosure requirements for easement holders including funding sources and foreign capital interests; and whether Vermonters have a right to know when international capital has a financial interest in Vermont land. No written response was received.

Q11. Vermont Sovereignty Over Vermont Land

What the public record shows:

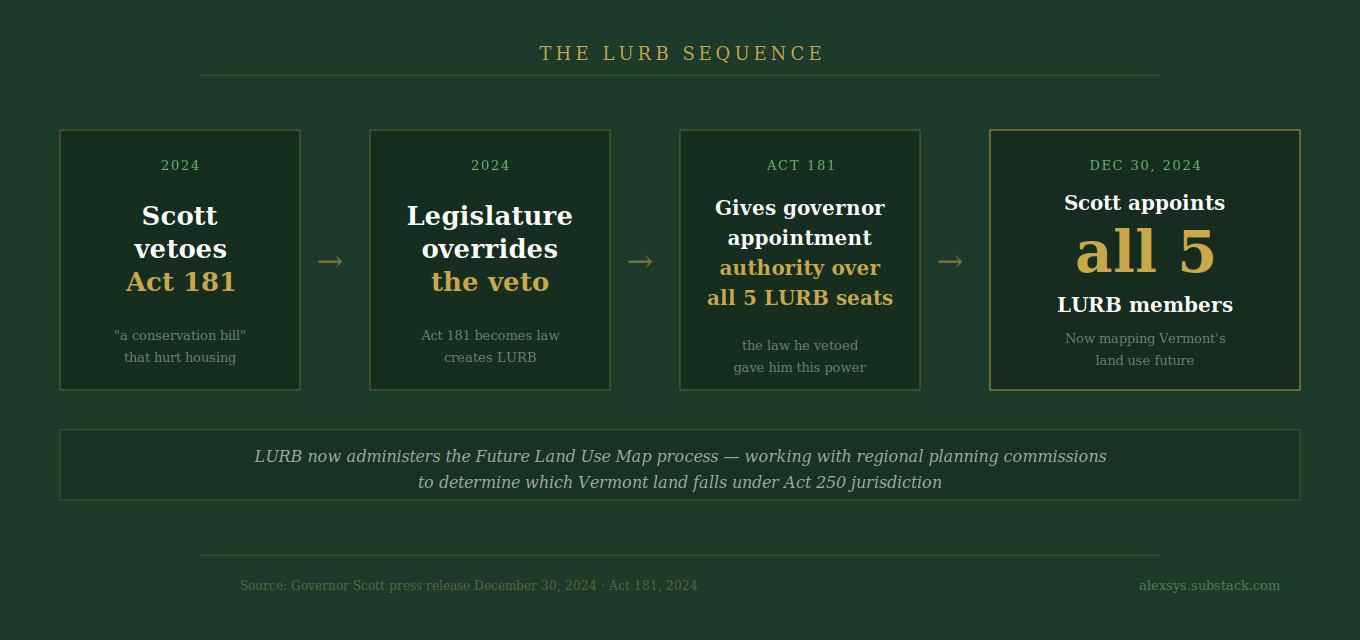

Scott vetoed Act 181 in 2024, citing concerns about regulatory overreach and impact on rural communities and property owners. The Legislature overrode the veto.

Act 181 created the Land Use Review Board and gave the governor appointment authority over all five seats. Scott appointed all five LURB members on December 30, 2024, effective January 1, 2025: Janet Hurley (Chair), Alex Weinhagen, L. Brooke Dingledine, Kirsten Sultan, and Sarah Hadd. Scott’s stated rationale: “I’m confident this board has the diverse expertise, work ethic, and passion to tackle the work that’s required in Act 181 while also forwarding common sense improvements to the law to further our shared goals.”

LURB is now the body tasked with the tier system mapping process — determining which Vermont land falls under Act 250 jurisdiction, what constitutes Tier 3 critical natural resources areas, and what areas receive additional protections. The board works directly with regional planning commissions on the Future Land Use Map process.

The LURB Nominating Committee that screened candidates included Scott’s Deputy Chief of Staff Brittney Wilson as his designated representative, alongside legislative members including Rep. Amy Sheldon, the House sponsor of Act 181.

Scott signed an executive order relaxing wetlands buffers in state-designated growth areas. LCAR rejected the resulting rule 5-3 on May 21, 2026.

Scott allowed Act 59 to become law without his signature in 2023.

S.325, a partial repeal of Act 181 repealing the Road Rule, Tier 2 Area Report, and Tier 3 provisions, passed the Vermont Legislature 28-2 in the Senate on May 27, 2026. As of June 10, 2026, the bill does not appear on the governor’s signed bills list, the Acts and Resolves list, or the enacted-without-signature list at legislature.vermont.gov. The bill’s status as of publication is pending. Vermont Investigative will update when action is confirmed.

Scott’s public record shows consistent opposition to expanding state regulatory control over private land use decisions — while simultaneously exercising the appointment authority over the board administering that regulatory system that Act 181 provided him.

No specific enforceable mechanism identified in the public record for ensuring rural Vermonters have binding input when international conservation frameworks shape Vermont land use and tax policy.

What was asked: What specific and enforceable mechanism ensures that rural Vermonters — farmers, foresters, landowners, working families — have meaningful and binding input when international conservation frameworks and globally-aligned economic models shape Vermont land use and tax policy. No written response was received.

Q12. Rural Vermont Policy Framework

What the public record shows:

Scott’s budget address describes CHIP as opening “the door for rural and smaller communities across Vermont to access a financing tool that has historically been out of reach.”

His budget proposes extending Act 250 interim housing exemptions to smaller towns, repealing the Road Rule, and making VHIP funding permanent, all framed as disproportionately beneficial to rural Vermont.

No public record found of Scott acknowledging that the policy architecture currently being built in Montpelier systematically disadvantages rural Vermont.

What was asked: His specific policy commitment to rural Vermont as a fiscal and regulatory framework; what his administration does differently for a town of 400 in Essex County versus Burlington; and whether he acknowledges the current policy architecture systematically disadvantages rural Vermont. No written response was received.

Q13. Data Centers — Energy, Land, and Rural Impact

What the public record shows:

May 18, 2026: Scott signed Executive Order 04-26 establishing the Vermont AI Economic Taskforce, directing a sector-by-sector economic assessment of AI’s impact on Vermont with emphasis on rural counties experiencing the largest contraction in working-age population.

May 28, 2026: Scott vetoed H.727, the Vermont Sustainable Data Centers Act — confirmed on the governor’s official 2026 legislative actions page (governor.vermont.gov, updated June 8, 2026). The bill had passed the Senate 26-3 and the House on a near-unanimous voice vote. His veto message: “We cannot afford policies that risk driving current or future jobs and investment to other states, when we already have regulations and policies in place to address our concerns about data centers.”

He cited Vermont’s Act 250 process, Public Utility Commission oversight, environmental permitting, energy siting rules, and municipal zoning as sufficient existing regulatory authority.

May 29, 2026: The House attempted to override the veto, falling short 83-52 with 90 votes needed. The override broke along party lines — the only partisan vote on a bill that had passed with tripartisan support in both chambers.

The Vermont Natural Resources Council documented that a single 20-megawatt facility — H.727’s minimum threshold — requires as much electricity as roughly 35,000 EVs, while Vermont had fewer than 21,000 EVs registered statewide as of January 2026.

What was asked: Whether he supports H.727 as passed, the stronger Senate version, or S.205’s moratorium approach; whether Vermont should actively recruit data centers; and what protections he would establish to prevent data center development from competing with agricultural land, rural water supplies, and Vermont’s housing construction workforce. No written response was received.

Q14. The Pricing Mismatch Question

What the public record shows:

Scott’s budget address and entire public record focus exclusively on supply-side interventions: regulatory reform, infrastructure financing, and new construction programs.

No public record found of Scott addressing the pricing mismatch question — whether Vermont’s housing problem is a supply shortage or a mismatch between asking prices and what working Vermonters can pay.

No public record found responding to market data showing inventory up 16% year over year, days on market up 22 days, 13.4% of homes experiencing price reductions, and a sale-to-list ratio of 96.3%.

What was asked: The evidence that Vermont’s housing problem is primarily a supply shortage rather than a pricing mismatch; and why policy focuses on new construction rather than making existing inventory accessible. Respond with data, not narrative. No written response was received.

Addendum A1. The Housing Math — Nine Years, $800 Million

What the public record shows:

Scott’s own budget address states approximately $800 million invested in housing since 2020. His own secretary Kurrle states Vermont is on track to build just over 12,000 of the 40,000 units needed by 2030 — 30% of the stated target.

The administration’s two flagship housing programs, by its own accounting: VHIP has produced more than 1,000 rental units over five years at $39,000 per unit. The Brownfields Revitalization Fund has produced 745 units across $23 million since October 2021. Combined: approximately 1,750 units from the programs Scott calls most effective.

The administration’s stated need is 40,000 units by 2030 — a figure derived from population growth projections that Q1 of this questionnaire asks Scott to reconcile with two consecutive years of Vermont population decline and rising housing inventory. Even accepting that figure at face value, the documented pace of the administration’s own best tools is approximately 350 units per year combined.

$800 million invested. 30% of a target the underlying math may not support. The gap is in the administration’s own numbers.

What was asked: Why the investment model is adequate to the scale of the problem he has described — or an acknowledgment that it is not, and identification of what structural change a sixth term would produce. No written response was received.

Addendum A2. The Tax Freeze — Fiscal Discipline or Fiscal Deferral?

What the public record shows:

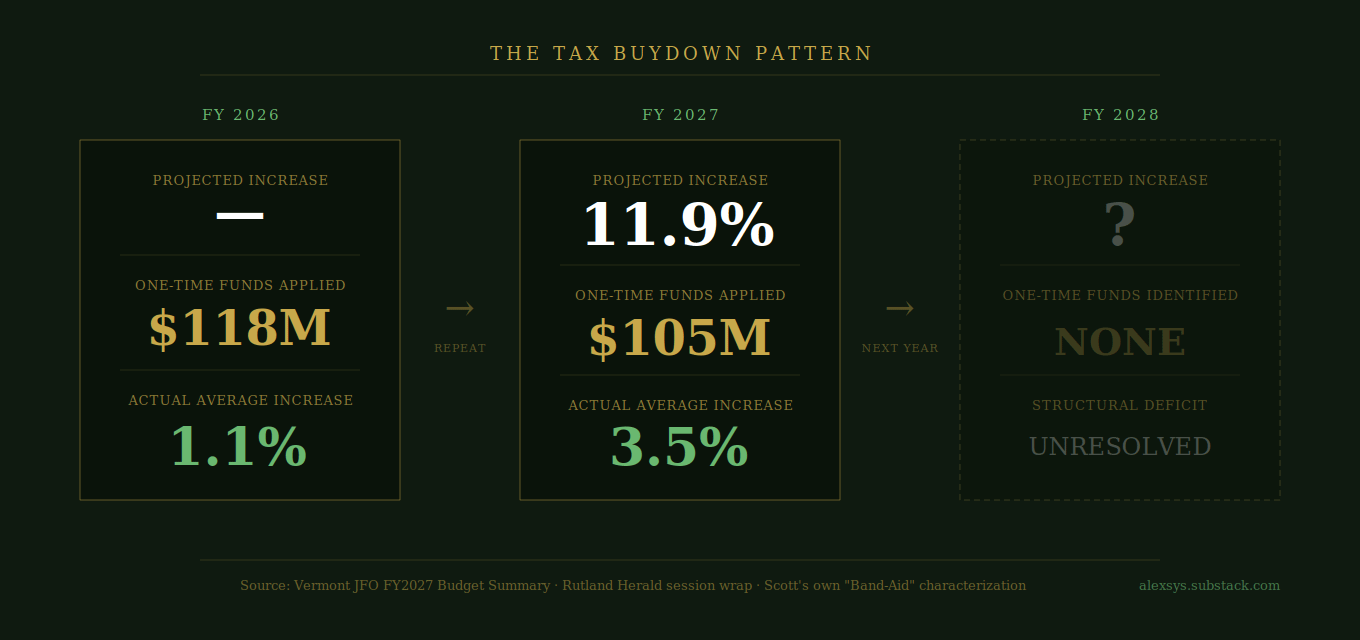

Spring 2024, before the November election: Scott and the legislature applied approximately $118 million in one-time funds — $77.2 million one-time General Fund and $41 million Education Fund surplus, per JFO — to hold the FY2026 average education property tax increase to approximately 1.1%.

December 1, 2025: The Department of Taxes projected an average increase of 11.9% for FY2027. Vermont Tax Commissioner Bill Shouldice said at a media briefing: “The rate of increase that we’re talking about is simply unacceptable and certainly defines unaffordability.” Approximately half of that projected increase was directly attributable to the prior year’s one-time funds no longer being available.

Two consecutive fiscal years document the pattern: FY2026, approximately $118 million in one-time funds applied before the November 2024 election, average increase held to 1.1%; FY2027, approximately $105 million in one-time funds applied through H.949 — $104,908,098 per the FY2027 Budget Summary, page 11 — bringing the average statewide increase to approximately 3.5%, per Rutland Herald end-of-session coverage and Lake Champlain Chamber session summary, June 2026. Of that $105 million, approximately $52.45 million was reserved in the Education Fund to help offset FY2028 increases — meaning the legislature partially deferred the pattern Scott was pushing to repeat fully. FY2028, the structural deficit that produced the 11.9% projection in FY2027 remains unresolved beyond that partial reserve. Scott described the approach as a “Band-Aid” while arguing Vermonters need relief now.

What was asked: How applying one-time money to suppress a tax increase before an election — knowing it would produce a larger increase the following year — is consistent with the fiscal discipline he has campaigned on for nearly a decade. No written response was received.

Addendum A3. Act 73 and the Task Force — Who Is Accountable?

What the public record shows:

Act 73, signed by Scott in June 2025, established an 11-member School District Redistricting Task Force required to deliver up to three mandatory consolidation maps to the legislature by December 1, 2025. The maps, if adopted by the legislature, would have created new school districts of 4,000 to 8,000 students beginning in the 2028-2029 school year.

Appointment authority over task force members was distributed across multiple parties: the Governor, the Speaker of the House, and the Senate Committee on Committees each held appointment authority over designated seats.

On November 18, 2025, a majority of task force members voted to recommend a voluntary regional cooperation model — a Community Education Service Agency structure — rather than the mandatory consolidation maps the law required. No maps were delivered to the legislature.

Scott’s verbatim public statement, December 2025: “They didn’t redraw the lines, and they were supposed to put forward three maps for consideration, and they failed.”

A documented structural fact: even if the task force had delivered mandatory consolidation maps on December 1, 2025, Act 73’s implementation date for new school districts was 2028-2029. The task force outcome had no bearing on the 2026 property tax increase, which was driven by healthcare costs, inflation, and expiration of one-time subsidies — factors unrelated to district boundaries, per Vermont Agency of Education and JFO documentation.

The 2026 legislative session produced a voluntary consolidation framework rather than mandatory maps, passed with bipartisan support after Scott’s mandatory consolidation position became untenable. Scott accepted the voluntary framework as part of the end-of-session compromise.

No public record found of Scott addressing how he would deliver mandatory structural education reform in a sixth term given that the primary mechanism Act 73 created — the redistricting task force — produced a voluntary cooperation framework rather than the mandatory maps the law required.

What was asked: What responsibility his administration bears for the task force’s outcome, and what his path to delivering structural education reform looks like in a sixth term given the outcome of Act 73’s primary implementation mechanism. No written response was received.

Addendum A4. Act 59, Wetlands, and Land Sovereignty

What the public record shows:

Scott vetoed Act 181 in 2024 and vetoed noncitizen voting charter amendments in 2021 and 2023.

Scott signed an executive order relaxing wetlands buffers in state-designated growth areas. LCAR rejected the resulting rule 5-3.

Scott allowed Act 59 to become law without his signature in 2023.

After the Legislature overrode his Act 181 veto, Scott exercised the appointment authority that Act 181 provided him — appointing all five members of the Land Use Review Board on December 30, 2024. LURB is now administering the tier system mapping process, determining which Vermont land falls under Act 250’s jurisdiction and what constitutes Tier 3 critical natural resources areas. The board works directly with regional planning commissions on the Future Land Use Map process.

Vermont’s Act 59 conservation planning process has received federal funding tied to Biden-era international biodiversity commitments.

Scott’s March 2026 commentary “Vermont Can’t Conserve Working Lands by Undermining Them,” published on governor.vermont.gov, argues that conservation and land use policy has been shaped by “paid advocates” with “disproportionate voice” and that “no more decisions about rural Vermont without rural Vermonters at the table.”

His support for H.70 — which would have counted Current Use working lands toward Act 59’s conservation targets — is the most concrete documented action in his record directed at ensuring working landowners benefit from Act 59 goals.

No public record found of Scott identifying a specific enforceable mechanism to ensure Vermont land use policy is driven by Vermont landowners rather than federal grant conditions or international policy frameworks.

What was asked: What specific actions he has taken — or would take in a sixth term — to ensure Vermont land use policy is driven by Vermont landowners and communities rather than by federal grant conditions, conservation organization priorities, or international policy frameworks. No written response was received.

Addendum A5. The Unmapped Wetlands Claim

What the public record shows:

May 15, 2026, Governor Phil Scott’s verified Facebook page (facebook.com/share/p/1Bhykq7Agv/): “Specifically, the Scott Administration’s proposal (which will be administered according to the Governor’s executive order) would allow for the construction and rehabilitation of more housing units in areas already designated for housing, without reducing a single square inch of wetlands in Vermont.”

Vermont Department of Environmental Conservation, Final Proposed Filing to LCAR, 25-P040, April 8, 2026: the rule makes housing construction an allowed use in unmapped Class II wetlands in areas designated for growth, and removes regulatory protection for Class II wetlands not shown on the Vermont Significant Wetlands Inventory map — including wetlands contiguous to mapped areas.

DEC’s own filing acknowledges the VSWI maps are “mostly created by looking at aerial photos, not by visiting the site” and “often do not show the exact boundaries of wetlands and usually show wetlands as smaller than they really are.”

LCAR rejected the rule 5-3 on May 21, 2026.

A wetland that does not appear on an incomplete aerial-photo-based map is still a wetland.

What was asked: Whether his public statement referred only to mapped wetlands — and if so, why that distinction was not made in the public statement. No written response was received.

What Remains Unanswered

Vermont Investigative transmitted nineteen questions to Governor Scott’s office — fourteen master questions asked of all statewide candidates and five candidate-specific addendum questions drawn from his public record and stated positions. No written response was received to any of them.

Where the nine-year public record of his administration addresses a question, this piece documents what it shows. Four specific questions found no public record response after extensive review: whether Scott supports carbon markets or biodiversity offset markets to fund Act 59 conservation goals; what restrictions he would apply to foreign institutional investment in Vermont land or conservation easements; whether he supports public disclosure requirements for conservation easement holders and their funding sources; and what specific enforceable mechanism would ensure Vermont land use policy is driven by Vermont landowners rather than federal grant conditions or international policy frameworks when those conflict.

Two bills remain pending as of publication with no gubernatorial action confirmed: S.190, the reference-based pricing healthcare bill, and S.325, the Act 181 partial repeal. Vermont Investigative will update both sections when action is taken.

This piece will be updated if written responses are received.

Prior Financial Record

DuBois Construction and ethics record

Scott co-owned DuBois Construction, a Middlesex firm that regularly contracted with the state, for approximately 30 years. In December 2016 he sold his 50% stake back to the company for $2.5 million, self-financed at 3% interest over 15 years — leaving him as DuBois’s largest creditor while governor.

October 2018: The Vermont State Ethics Commission ruled the arrangement violated the state code of ethics: “The public official has a conflict of interest because he is financially intertwined as a creditor, who has an ongoing financial interest in a company that contracts with the State, which the public official as governor is the chief executive officer.” The commission’s first executive director subsequently resigned, stating the commission had exceeded its authority. In September 2019, the commission withdrew the opinion — not on the merits, but on procedural grounds: VPIRG, which had requested the opinion, was not an authorized requestor under the commission’s rules. The DuBois/creditor conflict finding was never addressed on the merits.

This is the only documented Ethics Commission action involving Scott. Vermont Investigative found no other ethics findings, complaints, or enforcement actions against him in any year from 2017 through 2025.

2022: DuBois sold to Barrett Trucking. Wayne Lamberton, DuBois VP and close associate of Scott, stated Scott’s debt obligation “will be satisfied.” The final disposition of the $2.5 million debt has not been confirmed in any public document. Scott’s 2026 financial disclosure shows no outstanding loans or receivables requiring disclosure.

Wayne Lamberton contribution record — verified from Vermont campaign finance database

2016: $2,000 (January) + $2,000 (July) = $4,000

2018: $4,000 maximum

2022: $4,000 maximum — same cycle DuBois was sold to Barrett Trucking

2024: $0 to Scott

Total verified: $12,000 across four cycles

The Standard Applied

Vermont Investigative applies the same sourcing standard to every candidate regardless of party, office, or incumbency. Every claim in this piece points to a primary document filed by the Scott administration, a statement made voluntarily in a public forum, or a filing retrieved from the Vermont Secretary of State, Vermont Joint Fiscal Office, or Vermont Legislature.

No inference has been drawn beyond what the documents show. No intent has been attributed. No villain has been constructed.

Vermont voters are entitled to the documented record before they vote on August 11.

Sources

Filed with Vermont Secretary of State, May 26, 2026 — Phil Scott 2026 Financial Disclosure Form — Philip B. Scott and Diana McTeague Scott IRS Form 1040, tax year 2025 — Phil Scott Campaign Finance Disclosure Statement, 2026 Mar 15 Disclosures, Filing Entity ID 33545

Governor’s Office — governor.vermont.gov — FY2027 Budget Address, January 20, 2026 — CHIP Program Launch press release, February 2, 2026 — Brownfield Revitalization Fund press release, February 5, 2026 — Executive Order 04-26, Vermont AI Economic Taskforce, May 18, 2026 (primary document on file) — LURB Appointments press release, December 30, 2024 — Action Taken on Bills During the 2026 Legislative Session, updated June 8, 2026 (screenshots on file) — Sam Lincoln commentary, “Vermont Can’t Conserve Working Lands by Undermining Them,” March 26, 2026, governor.vermont.gov/governor-scotts-blog/commentary-vermont-cant-conserve-working-lands-undermining-them

Veto Messages — H.727, sustainable data center deployment, May 28, 2026 — S.218, chloride contamination of state waters, May 6, 2026 (primary document on file) — Act 181, 2024 — Burlington noncitizen voting charter amendment, May 2023

Rulemaking — Vermont Department of Environmental Conservation, Final Proposed Filing to LCAR, 25-P040 Vermont Wetland Rules, April 8, 2026, legislature.vermont.gov

Social Media — Governor Phil Scott verified Facebook page, facebook.com/PhilScottforVermont — May 15, 2026 post (”THERE THEY GO AGAIN,” wetlands), facebook.com/share/p/1Bhykq7Agv/ (screenshot on file, documented June 2026)

Fiscal Record — Vermont Legislative Joint Fiscal Office, FY2027 Budget Summary, ljfo.vermont.gov — Vermont Legislative Joint Fiscal Office, Education Finance Update, All Legislative Briefing, December 3, 2025, Julia Richter, Principal Fiscal Analyst — VTDigger, Ethan Weinstein, “Nearly 12% property tax increase projected for next year,” December 1, 2025

Campaign Finance — Vermont campaign finance database, contributor search “Lamberton,” campaignfinance.vermont.gov, retrieved June 9, 2026 — Vermont campaign finance database, Phil Scott 2024 General Election profile, retrieved June 9, 2026

Legislative Record — Act 59 of 2023 (H.126), Vermont Community Resilience and Biodiversity Protection Act, legislature.vermont.gov — S.190 bill status page, legislature.vermont.gov/bill/status/2026/S.190 — S.325 bill status page, legislature.vermont.gov/bill/status/2026/S.325 — H.289, An act relating to affordable climate initiatives, introduced February 2025, legislature.vermont.gov — Act 250 LURB Nominating Committee page, act250.vermont.gov/land-use-review-board-nominating-committee

Education Reform Record — Vermont Agency of Education, Act 73 Summary page, education.vermont.gov — Vermont School Boards Association, Act 73 Education Transformation page, vtvsba.org — Valley News, “Editorial: Scott should put forward detailed education reform plan,” December 5, 2025 (Scott quote: “They didn’t redraw the lines”)

Ethics Record — Vermont Public, “Scott’s Business Ties Violate State Code of Ethics, Commission Says,” October 2, 2018 — VTDigger, “Ethics Commission withdraws opinion critical of Gov. Scott,” September 5, 2019 (documents procedural reversal and executive director resignation) — VTDigger, “Company that owed Gov. Phil Scott $2.5 million is sold,” February 14, 2022

Social Media (additional) — Governor Phil Scott verified Facebook page, May 12, 2026 post (H.70/Current Use working lands). Screenshot on file, documented June 2026.

News Coverage Referenced — Lindsay Kurrle, “Kurrle: More work ahead on Vermont’s housing crisis,” VermontBiz, September 14, 2025 — VTDigger, Shaun Robinson, “Gov. Phil Scott unveils $9.4 billion state budget proposal,” January 20, 2026 — Vermont Public, “VTrans layoffs proposed as part of Gov. Phil Scott’s state budget,” January 21, 2026 — Vermont Public, Liam Elder-Connors, “Democrats want to expedite hospital pricing reforms,” May 28, 2026 — Vermont Public, Lexi Krupp, “UVM Health Network announces layoffs, over $180M in cuts,” July 29, 2025 — VTDigger, Olivia Gieger, “UVM Health cuts 142 jobs — an estimated $9 million in staff positions,” June 9, 2026 — Vermont Public, “With major changes to Act 250 underway, a new board takes the reins,” January 2, 2025 — Mychamplain Valley, “Vermont Supreme Court affirms non-citizens voting in school elections,” May 15, 2026 — VTDigger, “Phil Scott vetoes noncitizen voting in Burlington,” May 27, 2023 — VTDigger, “Environmentalists celebrate as Phil Scott allows conservation bill to become law without his signature,” June 12, 2023 — Vermont Public, “To tax a second home, first you have to define it,” April 30, 2025 — Vermont Public, “With a deal on education reform in hand, Vermont lawmakers close out the session,” May 29, 2026 — Rutland Herald, “Boots on the Ground: End of the session,” June 2026, rutlandherald.com — Lake Champlain Chamber, “Advocacy Update — Session Summary 2026,” June 2026, lccvermont.org — Campaign for Vermont, “REVIEW: FY2027 Property Tax Yield Bill (H.949),” March 2026, campaignforvermont.org

Questionnaire Transmission — Vermont Investigative master questionnaire transmitted May 16, 2026 to press@governor.vermont.gov and amanda.wheeler@vermont.gov. Both transmissions documented. No response received as of publication.

Update: The Waterbury Office Leases

Updated June 11, 2026

Vermont Investigative has completed verification of a state contracting matter identified during the research for this piece.

What the primary documents show:

In August 2025, the Scott administration announced a return-to-office mandate requiring approximately 3,000 state employees to work in person at least three days per week beginning December 1, 2025. The Agency of Human Services, which operates largely out of the Waterbury State Office Complex, faced a documented shortage of office space to accommodate the returning workers. In October 2025, hundreds of AHS employees demonstrated at the Waterbury complex to show lawmakers and the public that there were not enough desks to accommodate the mandate.

On November 17, 2025 — two weeks before the mandate took effect — the State of Vermont, Department of Buildings and General Services signed three leases with Malone Superior LLC for office space at Pilgram Park in Waterbury, to be occupied by the Agency of Human Services. The leases are primary documents filed by the state and on file with Vermont Investigative:

Lease 10045 — 5,399 square feet, 93 Pilgram Park Condominiums, Suite 6, second floor. Year 1 annual rent: $107,980. Five-year total: approximately $553,373.

Lease 10046 — 4,257 square feet, 5 Pilgram Park Condominiums, Suite 2, first floor. Year 1 annual rent: $85,140. Five-year total: approximately $452,093.

Lease 10047 — 12,016 square feet, 5 Pilgram Park Condominiums, Suite 5, second floor. Year 1 annual rent: $240,320. Five-year total: approximately $1,275,099.

All three leases run December 1, 2025 through November 30, 2030. Combined square footage: 21,672 square feet. Combined five-year value: approximately $2.28 million. All rental payments directed to Malone Superior LLC, 338 River Street, Unit 7, Montpelier, VT 05602.

Vermont Investigative retrieved the Vermont Secretary of State business registration for Malone Superior LLC on June 10, 2026. Record #296047 confirms the company is a domestic LLC active in good standing, registered October 9, 2014, with a stated business purpose of nonresidential property management (NAICS 531312). The filing lists three members: Wayne Lamberton, 213 Paine Turnpike North, Montpelier; Patrick Malone, 338 River Street, Unit 7, Montpelier; and Randy Lague, 213 Paine Turnpike North, Montpelier.

Wayne Lamberton’s verified contributions to Phil Scott campaigns, from the Vermont campaign finance database: $2,000 (January 2016), $2,000 (July 2016), $4,000 maximum (February 2018), $4,000 maximum (October 2022) — $12,000 total across four cycles. Lamberton made no contribution to Scott in 2024.

On April 1, 2026, the Vermont Labor Relations Board ordered the Scott administration to rescind the return-to-office mandate, ruling the state had “refused to bargain in good faith and interfered with employees’ exercise of rights.” Scott called the decision “disappointing” and said his administration would appeal to the Vermont Supreme Court. On May 8, 2026, the labor board declined to pause its order.

The three Pilgram Park leases with Malone Superior LLC remain active through November 30, 2030. The mandate that created the documented need for the space has been ruled unlawful.

Vermont Investigative documents the sequence. No inference is drawn beyond what the primary documents show.

Sources for this update: Vermont Secretary of State, Malone Superior LLC, Record #296047, retrieved June 10, 2026. bizfilings.vermont.gov. State of Vermont leases 10045, 10046, 10047 — Department of Buildings and General Services / Malone Superior LLC, executed November 17, 2025. Primary documents on file. VTDigger, Ethan Weinstein, “Vermont state employees show up in person to demonstrate constraints of Waterbury office complex,” October 23, 2025. vtdigger.org. VTDigger, Shaun Robinson, “Vermont state employees’ union files labor complaint over Gov. Phil Scott’s return-to-work plan — and sues,” November 20, 2025. vtdigger.org. VTDigger, Theo Wells-Spackman, “Vermont labor board orders state to end return-to-office requirement for employees,” April 1, 2026. vtdigger.org. VTDigger, Theo Wells-Spackman, “Vermont labor board declines state’s request to pause order blocking return-to-office policy,” May 8, 2026. vtdigger.org. Vermont campaign finance database, contributor search “Lamberton,” campaignfinance.vermont.gov, retrieved June 9, 2026.

If you find this work useful, please consider supporting it with a Substack subscription or at ko-fi.com/alexsysthompson